IRS Revokes Tax Exemption For The Curtis Coleman Institute

by April 25, 2013 6:21 pm 328 views

Last month, I reported on issues surrounding the Curtis Coleman Institute for Constitutional Policy. At that time, the Institute’s tax exemption application was still pending before the IRS, which they said was due to a delay in the IRS processing. It seems their problems have compounded.

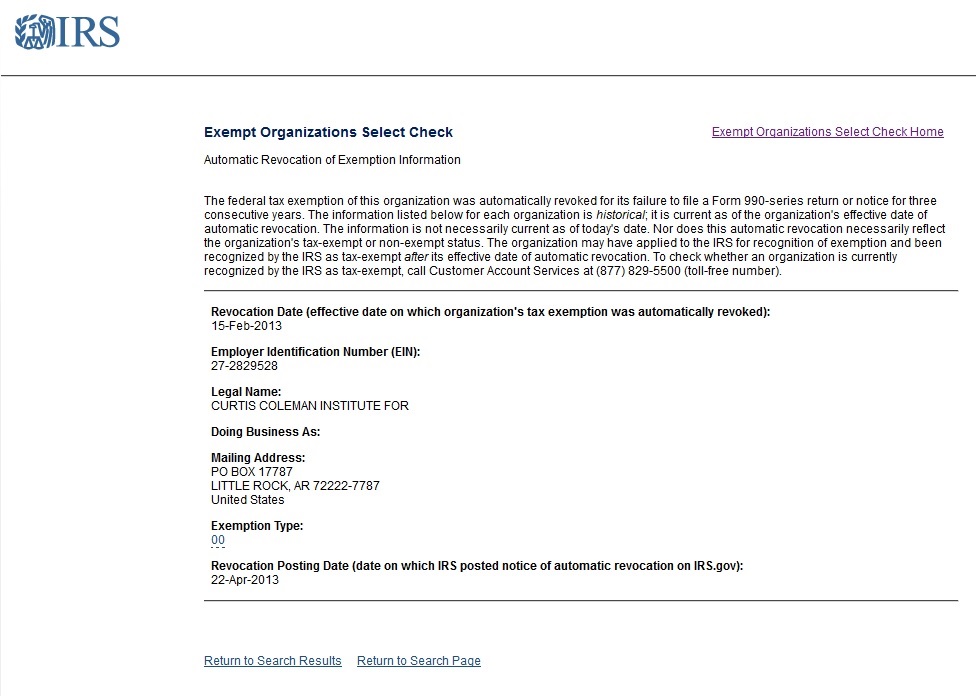

The Tolbert Report has learned that the IRS has revoked the tax exempt status of the Institute. The revocation was publicly posted on the IRS web site on April 22, 2013. According to the IRS, this was an automatic revocation due to a failure to file a Form 990 return for three consecutive years. The effective date of the revocation was the due date for the annual return that was due February 15, 2013.

{kind=link}

An annual return is required of tax exempt organizations even during the application process. The Institute was formed in June 2010 but did not apply for tax exempt status in until February 2012. In March of this year, an attorney for the Institute explained that this is within the rules as the organization has 27 months after the end of the month in which you were legally formed.

The IRS confirmed that the Institute filed a form 990 with a filing date of the periods ending September 2010, September 2011, and September 2012 all with a filing date of March 13, 2013. Possibly of note, I had requested a copy of the Institute’s Form 990 filings, which are public documents, on February 20 and on March 5 shortly before the actual filing took place.

Copies of the filings were provided to The Tolbert Report on March 23 and can be seen here, here, and here. The Tolbert Report also requested copies of the annual returns directly from the IRS but was told the documents are “unavailable” although it is not clear exactly what this means. UPDATE – A spokesperson for the IRS explained that with the revoked status of the organization, the Form 990’s are no longer open to public inspection.

According to the IRS, if an organization has had its tax-exempt status automatically revoked and wishes to have that status reinstated, it must file an application for exemption and pay the appropriate user fee even if it was not required to apply for exempt status initially. A new application process would then begin again and if the organization was granted tax exempt status, a new determination letter would be granted most likely with an effective date of the reinstated exemption (unless the organization was able to show reasonable cause, which seems unlikely).

The IRS would not confirm if the application was still pending at the time of revocation as the application is not a matter of public record until the tax exempt status is granted. However, since the IRS would not confirm this, it tells me that most likely the tax exempt status was not granted otherwise it would have been public record.

If this is the case – that the revocation took place before the tax exempt status was granted – then in essence the Institute was never a tax exempt organization. This is a problem not only for the Institute, but any donors that have claimed a tax deduction. The Institute advised its donors on its website – “Both personal and corporate contributions to The Institute are tax-deductible.” According to the annual return provided by the Institute, the organization has received $171,449 in gift, grants, contributions, and membership fees through September 20, 2012.

As of posting time of this story on Thursday, the Institute website was open to receive donations with the advice that the donations are tax-deductible.

The revocation of tax exempt status obviously also adds to the other issues I raised in March such as the fact they had not filed with the Arkansas Attorney General’s office and are not collecting sales tax on sales of their DVDs.

Talk Business has contacted the Institute for comment and will update this story if they respond.